Egypt E-Health and Teleconsultation Platforms Market Outlook 2024-2030: Forecast

Executive Summary

Egypt's e-health and teleconsultation market reached USD 1.1 billion in 2024, and the growth lever is integration. Smartphone access and the national Universal Health Insurance rollout are pulling telehealth from startup novelty into mainstream care.

Key Market Velocity Data

- Current Market Value: USD 1.1 billion in 2024

- Projected Market Value: approximately USD 2.2 billion by 2030

- CAGR: about 12% during 2025 to 2030

- Dominant Segment: video consultation, hospital-led

- Primary Growth Catalyst: smartphone access, insurance integration, and Vision 2030 investment

What Is Driving the Market?

Access and policy drive demand. With smartphone penetration near 65% and around 65 million users, the market sits at USD 1.1 billion in 2024 and is projected toward USD 2.2 billion by 2030 at about 12% CAGR. Over 5 million teleconsultations now happen annually. The under-served chronic-care population is the largest untapped demand pool, and adoption that began during the pandemic has become a permanent urban habit.

Government integration is the multiplier. Egypt has invested over USD 200 million in digital health under Vision 2030, and the Universal Health Insurance System covers more than 50 million citizens. Linking telehealth to insurance turns occasional use into reimbursed, recurring care. Reimbursement is the difference between a one-time download and a retained patient. Public-private partnerships are emerging to deliver telehealth at national scale.

- Access: about 65% smartphone penetration and 65 million users widen the patient base

- Demand: more than 5 million teleconsultations occur annually and are rising

- Government push: over USD 200 million in digital health investment under Vision 2030

- Insurance link: Universal Health Insurance covering 50 million-plus citizens makes telehealth reimbursable

Which Entities Are Shaping the Market?

A dense startup ecosystem leads. Vezeeta, with 21,000 licensed doctors across 41 specialties, anchors consultations, while Altibbi, Estshara, and Shezlong cover general and mental health. Pharmacy platforms Chefaa and Yodawy extend into e-prescription across the USD 1.1 billion market. These platforms compete on doctor-network depth and prescription fulfillment speed.

Specialist and diagnostic players round it out. Rology in teleradiology, Clinido, SehhaTech, DabaDoc, and Tabibi serve clinics and hospitals, while AXA Egypt links insurance. Hospitals are the dominant end-user, and video consultation leads by type across the USD 1.1 billion market growing about 12%. Consolidation is likely as funding tightens and integration costs rise.

Regulation is formalizing fast. The Ministry of Health and Population issued National Telehealth Guidelines in 2023, setting licensing, data-privacy, and quality standards. All platforms must increasingly sync with the Universal Health Insurance System covering 50 million-plus citizens, raising the compliance bar. Data localization and privacy rules add cost but build the patient trust adoption needs.

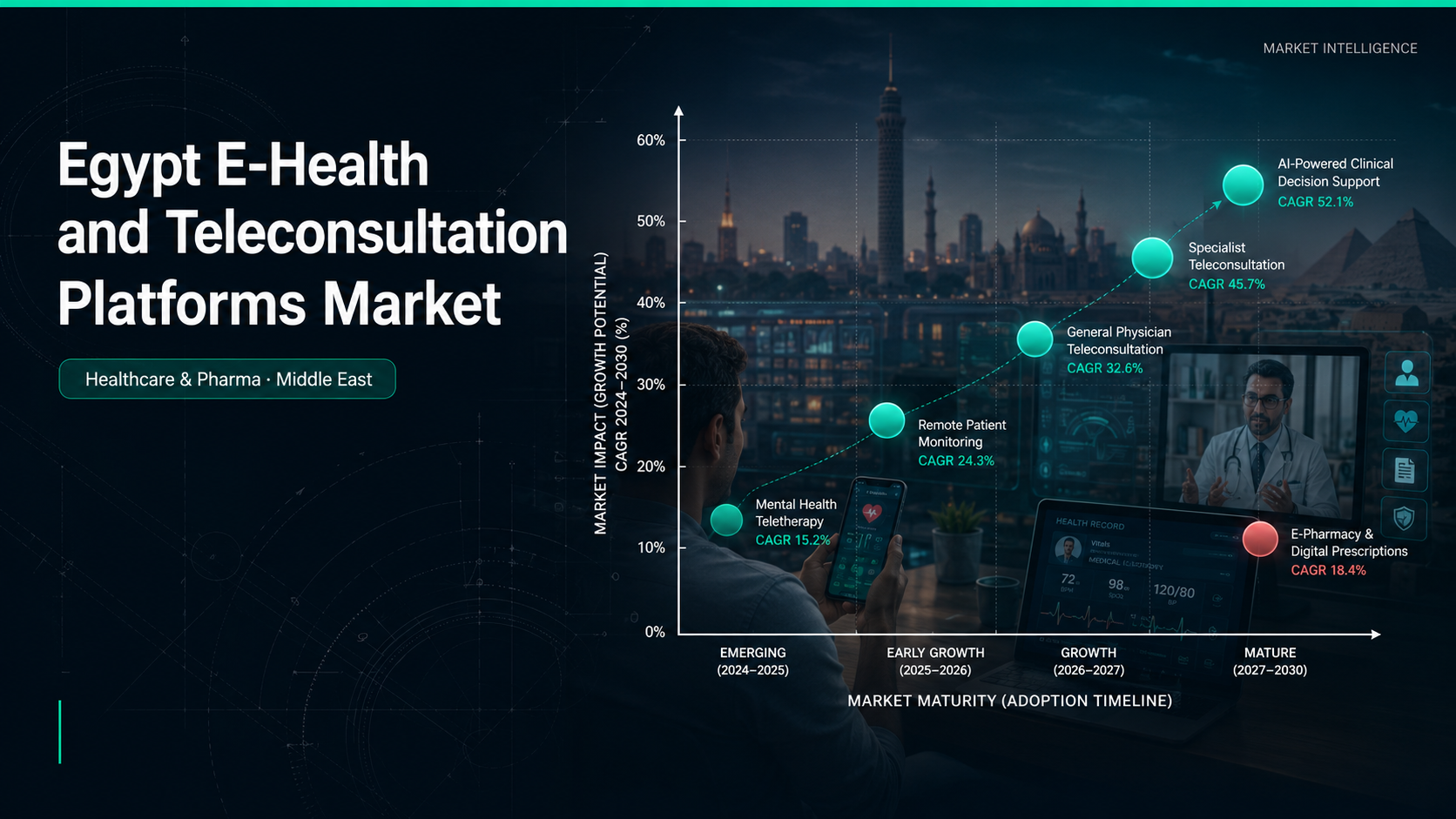

How Do Segments and Users Split?

Modes and users concentrate demand. Video consultation leads, ahead of chat-based, remote monitoring, mHealth, and e-prescription. Hospitals are the largest end-user, followed by clinics and individual practitioners, across the USD 1.1 billion market in 2024. Remote patient monitoring is the fastest-rising segment. Telepsychiatry and chronic-disease monitoring are emerging high-value niches. AI-assisted triage is starting to layer on top of standard video visits.

- By type: video consultation leads, with remote monitoring and e-prescription rising fastest

- By user: hospitals dominate, followed by clinics, practitioners, and insurers

- By driver: smartphone access and insurance integration anchor adoption

- By barrier: roughly 40% of rural Egypt lacks reliable internet, capping reach

What Does This Mean for B2B Decision-Makers?

Build for insurance integration, not just apps. The USD 1.1 billion market grows about 12%, but durable revenue comes from being inside the Universal Health Insurance System, not standalone consultations. Platforms that integrate with UHIS and hospitals will scale fastest. Whoever owns the patient relationship and data will dominate the next phase.

Rural reach is the constraint and the opportunity. With 40% of rural Egypt offline, low-bandwidth and chat-based models matter, while the 5 million-plus annual consultations prove urban demand. Compliance with the 2023 guidelines is now a prerequisite to operate. Arabic-language interfaces and local payment rails decide how deep adoption goes.

- For healthtech platforms: integrate with the Universal Health Insurance System for recurring, reimbursed care at national scale

- For hospitals: adopt teleconsultation to extend reach and cut outpatient load beyond connectivity-limited regions

- For investors: back platforms with insurance integration, licensed doctor networks, and strong patient retention rates

- For strategy teams: track the 2023 National Telehealth Guidelines shaping compliance and reimbursement

Ken Research Strategic Outlook

Ken Research sees Egypt e-health as an integration-and-insurance story, not a pure app race. The next phase rewards platforms that embed into the Universal Health Insurance System and hospital workflows while solving rural connectivity. Expect the USD 1.1 billion market to roughly double toward USD 2.2 billion by 2030 as digital health becomes mainstream, insurance-backed care.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Egypt E-Health and Teleconsultation Platforms Market Report

Comments

Post a Comment