Global IoT Warehouse Management Hits USD 13.7B at 8.3% CAGR on E-Commerce | Ken Research

Global IoT Warehouse Management Crosses USD 13.7B on E-Commerce Surge | Ken Research

The most disruptive force in global warehouse management is not robotics. It is the real-time data layer that makes robotics useful: IoT sensors, RFID networks, and edge computing that convert a warehouse from a storage facility into a predictive logistics engine. As per Ken Research market modelling, the global IoT warehouse management market is valued at USD 13.69 billion in 2024, with automation technologies reducing labor costs by up to 20% and real-time inventory management enabling a 15% increase in sales efficiency. The full competitive landscape and segment analysis are available in the Global IoT Warehouse Management Market Report.

This analysis draws on data from Ken Research market modelling, Grand View Research IoT benchmarks, EU Digital Operational Resilience Act (DORA) regulatory filings, and independent 3PL sector benchmarking.

USD 13.69 Billion in 2024: How Retail and E-Commerce Are Driving 8.3% CAGR Growth

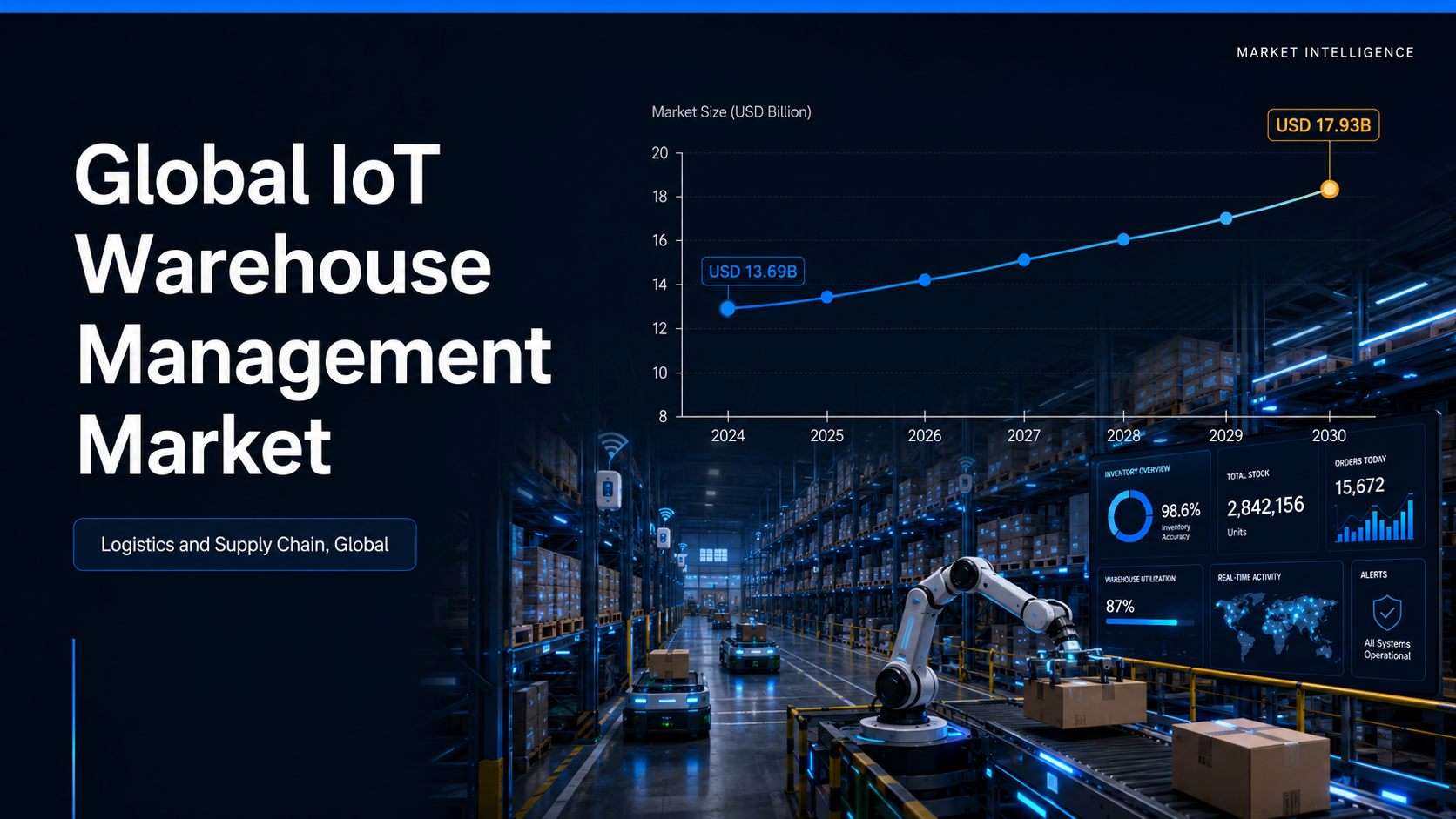

The global IoT warehouse management market is valued at USD 13.69 billion in 2024 and is projected to reach USD 17.93 billion by 2030 at an 8.3% CAGR. Retail and e-commerce is the dominant end-user segment, driven by global e-commerce reaching approximately USD 6.4 trillion, enabling warehouses to manage up to 50% more orders during peak seasons through IoT-enabled capacity scaling. Warehouse management software leads within the IoT stack, providing the data orchestration layer across RFID, sensors, and automated storage systems. For operators benchmarking regional IoT warehouse deployments, the Oman Smart Warehouse Robotics and IoT Analytics Platforms Market offers a direct GCC parallel where the same IoT stack is being deployed under Vision 2040 infrastructure mandates.

- Market Scale: USD 13.69 billion in 2024 to USD 17.93 billion by 2030 at 8.3% CAGR, per Grand View Research and Ken Research modelling.

- E-Commerce Driver: Global e-commerce at approximately USD 6.4 trillion, enabling warehouses to scale peak-season order capacity by up to 50% through IoT integration.

- Labor Cost Reduction: Automation and IoT devices reduce labor costs by up to 20%, with real-time inventory management delivering a 15% increase in sales efficiency.

How RFID, Cloud Computing, and Edge Analytics Are Reshaping 3PL Outsourcing Decisions

The shift from on-premise to cloud-based warehouse management systems is the most significant structural change in the sector, with cloud WMS platforms projected at USD 4 billion and smart warehouse solutions expected to reach USD 12 billion as standalone markets. Cloud-based platforms lower the capital barrier for 3PL outsourcing by eliminating hardware refresh cycles and enabling real-time supply chain consolidation across distributed facilities. The Kuwait Smart Warehouse IoT Analytics and Robotics Platforms Market demonstrates how cloud-first IoT deployments are accelerating 3PL outsourcing in GCC logistics hubs where last-mile fulfillment density justifies the capital investment.

- Cloud WMS: Projected at USD 4 billion, lowering capital entry barriers for mid-size 3PL operators and enabling multi-site IoT orchestration without hardware investment.

- Smart Warehouse Solutions: Expected to reach USD 12 billion as a standalone segment, combining IoT sensors with AI-powered analytics for predictive freight forwarding margins optimization.

Which IoT warehouse management providers are capturing market share as the USD 13.69B market consolidates around cloud-first platforms? Download Sample Report for competitive benchmarks and segment-level forecasts.

Why Are Cyberattacks Costing USD 3.86 Million Per Breach in IoT Warehouse Networks?

The same IoT data layer that makes warehouses efficient also makes them a cyberattack target. A 30% increase in cyberattacks on connected warehouse systems has raised the average breach cost to USD 3.86 million. EU DORA mandates digital technology standards for logistics operators, raising the compliance floor for IoT deployments across European supply chains. Initial investment exceeds USD 1 million for full IoT integration in mid-sized operations, concentrating deployments among tier-1 retailers and 3PLs with the capital infrastructure to absorb compliance costs alongside deployment expenses.

Global IoT Warehouse Management Outlook to 2030: North America Leads at 34.8% Share

North America holds the largest revenue share at 34.8% in 2024, driven by e-commerce fulfillment density and early IoT adoption among major retailers. Asia-Pacific is the fastest-growing region, propelled by rapid e-commerce scaling and manufacturing automation. Zebra Technologies, Honeywell Intelligrated, SAP SE, Oracle Corporation, Manhattan Associates, and Dematic lead the competitive landscape. The EU's Digital Operational Resilience Act guidelines are creating compliance-driven IoT upgrade demand across European logistics operators.

- Regional Leadership: North America leads at 34.8% revenue share in 2024; Asia-Pacific is fastest-growing on e-commerce and manufacturing automation adoption.

- Forecast: Market projected at USD 17.93 billion by 2030 from a USD 13.69 billion base in 2024 at 8.3% CAGR.

- Compliance Tailwind: EU DORA mandates digital technology adoption in logistics, driving IoT upgrade cycles across European 3PL operators and freight forwarding networks.

What 3PL Operators, Retailers, and Investors Must Do Before IoT Platform Consolidation Locks In Winners

The IoT warehouse management market is in a platform consolidation phase: cloud WMS leaders are securing multi-year contracts as operators prioritize supply chain consolidation over point-solution procurement. The USD 17.93 billion forecast by 2030 concentrates disproportionately in operators that commit to integrated IoT stacks now rather than maintaining legacy system integration complexity.

- 3PL Operators: Migrate to cloud WMS before the USD 4 billion cloud segment matures, locking in the 20% labor reduction cost advantage over legacy-system competitors.

- Retailers: Integrate RFID and IoT sensors to capture the 50% peak-season order capacity expansion that cloud-connected warehouses deliver over non-integrated competitors.

- Investors: Target cloud-native IoT warehouse platforms with DORA compliance certifications: EU regulatory tailwind creates contract moats worth USD 3.86 million per avoided breach.

Map the global IoT warehouse management competitive landscape and 2030 forecast by technology and end-user. Global IoT Warehouse Management Market Report covers provider analysis and regional growth forecasts.

Conclusion

The global IoT warehouse management market has reached the phase where the technology works and compliance frameworks are arriving together. The USD 13.69 billion base in 2024 and 8.3% CAGR through 2030 understate the real dynamic: cloud WMS adoption is creating platform lock-in that is very difficult to dislodge once multi-site supply chain data integrates. The strategic question for operators and investors is not whether to adopt IoT warehouse management: it is which vendor relationship survives the consolidation cycle. Access the Global IoT Warehouse Management Market Report for the full analysis.

Frequently Asked Questions

Q1: What is the size of the Global IoT Warehouse Management Market?

The Global IoT Warehouse Management Market is valued at USD 13.69 billion in 2024 and projected to reach USD 17.93 billion by 2030 at an 8.3% CAGR. North America leads with 34.8% revenue share while Asia-Pacific is the fastest-growing region on e-commerce and manufacturing automation.

Q2: Who are the key players in the Global IoT Warehouse Management Market?

Leading players include Zebra Technologies, Honeywell Intelligrated, SAP SE, Oracle, Manhattan Associates, and Dematic (KION Group). Cloud WMS is projected at USD 4 billion as a standalone segment, with smart warehouse solutions reaching USD 12 billion as operators consolidate on integrated stacks.

Q3: What is driving growth in the Global IoT Warehouse Management Market?

Three drivers dominate: global e-commerce reaching USD 6.4 trillion enabling 50% peak-season order capacity expansion, labor cost reduction of up to 20% through automation, and EU DORA compliance mandates driving IoT upgrade cycles. Real-time inventory management delivers a 15% increase in sales efficiency across integrated deployments. See also the Qatar Warehouse Fire Protection and IoT Suppression Systems Market.

Q4: What are the main challenges in IoT warehouse management adoption?

High initial investment exceeding USD 1 million, a 30% increase in cyberattacks averaging USD 3.86 million per breach, and legacy system integration complexity limit adoption among smaller operators and regional 3PL providers without the capital and compliance infrastructure to absorb deployment costs.

Q5: How does EU DORA regulation affect the Global IoT Warehouse Market?

EU DORA, implemented in 2023, mandates digital technology adoption standards for logistics operators, creating compliance-driven IoT upgrade demand across European supply chains. This regulatory tailwind accelerates cloud WMS adoption, creating platform lock-in worth more than USD 3.86 million per avoided breach across the growing European operator base.

For the full competitive benchmarking, segment-level forecasts, and regional breakdown, access the Global IoT Warehouse Management Market Report from Ken Research, covering logistics and supply chain technology markets globally.

Comments

Post a Comment