Global TPE Films and Sheets Market Crosses USD 3.4Bn : Ken Research Finds Automotive Demand Driving Growth

Global TPE Films and Sheets Market Hits $3.4Bn in 2024: Ken Research Finds Automotive Demand Surging | Ken Research

Executive Summary

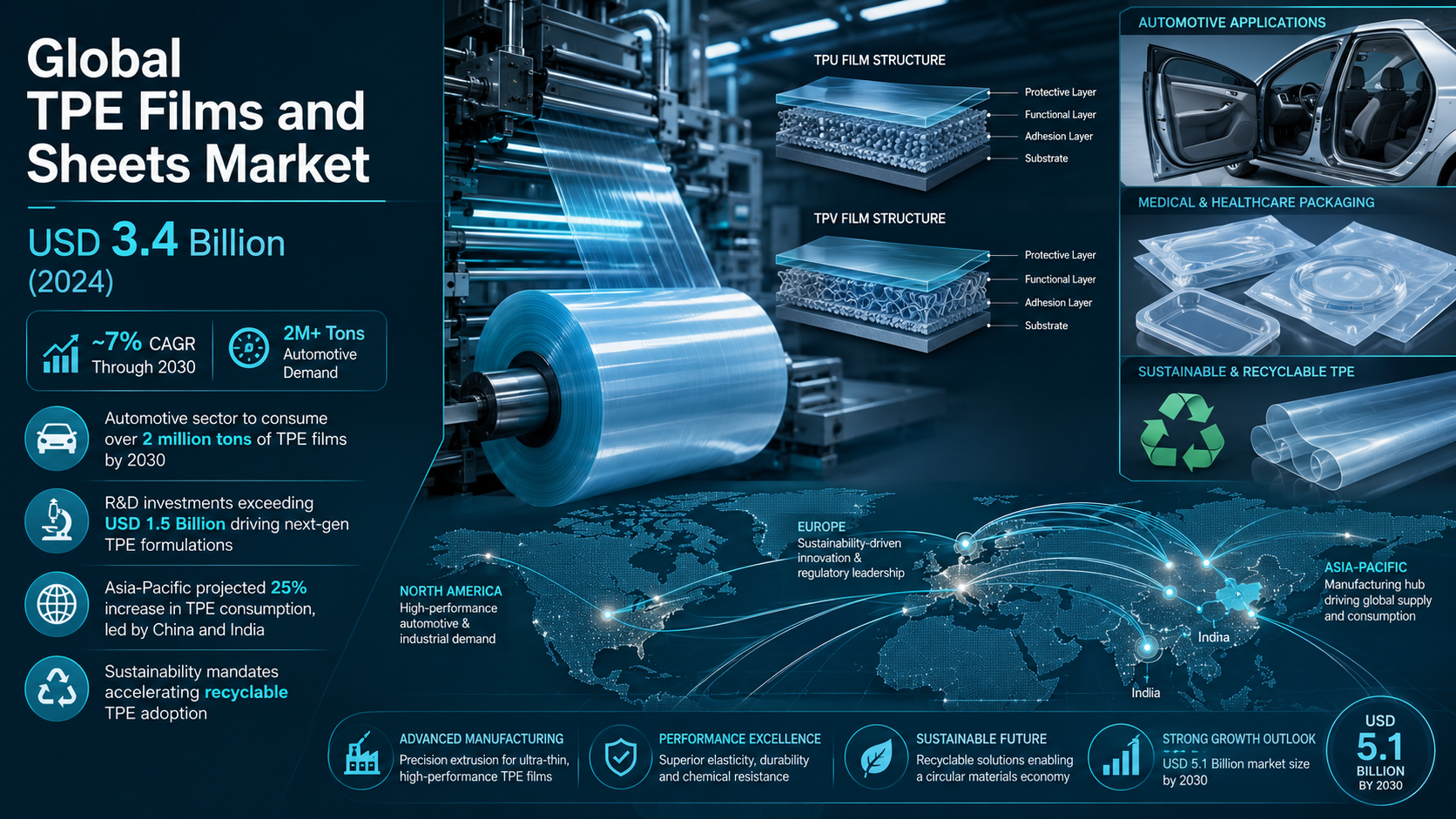

The Global TPE Films and Sheets Market reached a valuation of USD 3.4 billion in 2024, propelled by an accelerating shift toward lightweight, recyclable polymer materials across automotive, packaging, and medical end-use sectors. Growing at an estimated ~7% CAGR through 2030, the market is forecast to surpass USD 5.1 billion by the end of the decade, according to Ken Research. Asia-Pacific alone is projected to register a 25% increase in TPE consumption, anchored by manufacturing scale-ups in China and India. Amid tightening environmental mandates, including the EU Directive 2019/904 requiring recyclable plastics by 2030, thermoplastic elastomers are increasingly displacing traditional thermosets and rigid plastics across high-performance applications.

Key Takeaways

- Global TPE Films and Sheets Market valued at USD 3.4 billion in 2024, forecast to reach USD 5.1 billion by 2030

- Automotive sector projected to consume over 2 million tons of TPE films by 2030, driven by lightweighting and EV platform proliferation

- R&D investment in TPE product development exceeds USD 1.5 billion, with USD 600 million allocated specifically to next-gen film formulations

- Thermoplastic Polyurethane (TPU) leads by material type; automotive and packaging together represent more than 60% of end-use demand

- EU Directive 2019/904 mandates recyclable or reusable plastics by 2030, creating structural demand tailwinds for bio-based and recyclable TPE grades

- Asia-Pacific accounts for the fastest-growing regional trajectory, with a projected 25% consumption increase over the forecast horizon

Market At A Glance

- Base Year: 2024

- Market Size (2024): USD 3.4 billion

- Forecast Size (2030): USD 5.1 billion

- CAGR: ~7% (2025-2030)

- Historical Period: 2019-2024

- Geography: Global (US, Germany, China, Europe, Asia-Pacific)

- Leading Segment (Type): Thermoplastic Polyurethane (TPU)

- Leading End-Use: Automotive

- Key Regulation: EU Directive 2019/904; FDA compliance; EPA standards

Automotive and Packaging Sectors Drive Structural Demand Growth

The automotive industry stands as the primary consumption engine for TPE films and sheets globally, with sector demand projected to cross 2 million tons by 2030. Electric vehicle (EV) platform proliferation is a central catalyst, as automakers pursue aggressive lightweighting targets, replacing traditional rubber seals, interior films, and underbody protection materials with high-performance TPE grades. The broader lightweight materials market is projected to reach USD 300 billion globally, underscoring TPE's structural importance as a material of transition. Packaging, representing the second-largest end-use vertical, is simultaneously reshaping demand dynamics, with the global packaging market projected at USD 1.2 trillion, creating enormous volume potential for flexible, recyclable TPE films in food-grade, pharmaceutical, and industrial applications. Ken Research's analysis of the Global Fiber Reinforced Plastic Recycling Market highlights a parallel trend of advanced materials circularity gaining industrial traction.

- Automotive TPE film consumption forecast to exceed 2 million tons by 2030

- Global packaging market at USD 1.2 trillion, creating high-volume demand for flexible TPE films

- EV penetration rates in Europe and China driving replacement of vulcanized rubber with TPE-based alternatives across 4+ vehicle sub-systems

- Consumer goods and medical device packaging collectively represent the fastest-growing application niche within the non-automotive segment

Technology Innovation and R&D Investment Reshaping the Competitive Landscape

The Global TPE Films and Sheets Market is witnessing accelerating innovation cycles, with total R&D investment in the TPE sector exceeding USD 1.5 billion as of 2024, of which USD 600 million is specifically channeled toward film and sheet product development. Leading materials companies including BASF SE, Dow Inc., Kraton Corporation, Covestro AG, and Evonik Industries are investing in next-generation TPE formulations with enhanced barrier properties, improved UV resistance, and bio-based content. Thermoplastic Polyurethane (TPU) remains the dominant material type due to its superior mechanical properties and broad processability, while Thermoplastic Vulcanizates (TPV) and Styrenic Block Copolymers (SBC) are gaining ground in price-sensitive applications. Ken Research's research on the India Fine and Specialty Chemicals Market reflects how upstream raw material innovation is accelerating downstream applications in advanced polymer films. Similarly, the Global Automotive Thermal Management Market reveals adjacent opportunities where TPE films serve as critical functional components.

- Total TPE sector R&D investment exceeds USD 1.5 billion; USD 600 million dedicated to film/sheet product lines

- TPU leads material type segmentation due to 30%+ greater tensile strength versus standard thermoplastic olefins

- Bio-based TPE grades growing at approximately 2x the rate of conventional grades amid circular economy mandates

- More than 22 global players actively compete in the TPE films and sheets space, signaling a moderately consolidated competitive structure

Regulatory Frameworks and Sustainability Mandates Accelerating Market Transformation

Regulatory pressure is functioning as a structural market accelerant for recyclable and bio-based TPE films globally. The EU Directive 2019/904 mandates that all single-use plastic items must be recyclable or reusable by 2030, directly benefiting TPE film producers who can demonstrate closed-loop recyclability. FDA compliance requirements govern TPE films used in food contact packaging across North American markets, ensuring high barriers to entry and premium pricing for certified-grade products. Environmental Protection Agency (EPA) standards in the United States similarly require documented lifecycle analysis for industrial polymer films, creating compliance-driven demand for verified recyclable TPE solutions. The biodegradable plastics market, a structural adjacent to recycled TPE, is currently valued at USD 8 billion, reflecting the scale of sustainability-driven materials transition underway. Ken Research analysis of the Saudi Arabia Thermal Insulation Materials Market and Australia PVC Pipes Market each demonstrate how sustainability regulations are reshaping polymer material procurement decisions across geographies.

- EU Directive 2019/904 mandates recyclability by 2030, structurally favoring TPE over conventional thermoset films

- FDA and EPA compliance requirements add 15-20% cost premium for certified food-contact and industrial TPE films, protecting margins for compliant producers

- Biodegradable plastics market at USD 8 billion demonstrates growing end-market appetite for sustainable polymer alternatives

- ISO certifications now required by 85%+ of automotive OEM procurement contracts for polymer film suppliers

Asia-Pacific Emerges as the Dominant Growth Region Through 2030

Asia-Pacific is projected to deliver the strongest regional growth trajectory for TPE films and sheets through 2030, with a forecast 25% increase in regional TPE consumption driven by China's expanding automotive and electronics manufacturing base and India's emerging pharmaceutical packaging sector. China accounts for the largest production capacity in TPE films globally, benefiting from integrated petrochemical feedstock availability and strong government support for advanced materials manufacturing under national industrial policy frameworks. Japan and South Korea contribute precision-grade TPE film production for semiconductor and medical device applications, where exacting quality standards command significant pricing premiums. The region's favorable manufacturing cost structure, combined with growing domestic consumption across automotive, consumer goods, and medical packaging verticals, positions Asia-Pacific to capture more than 40% of incremental global TPE films demand growth through 2030. Ken Research's coverage of the Malaysia Smart Manufacturing and Industry 4.0 Market and Indonesia Advanced Wound Care Market illustrates adjacent industrial megatrends accelerating TPE adoption across the region.

- Asia-Pacific projected 25% increase in TPE consumption through 2030, outpacing all other regions

- China leads global TPE film production capacity, accounting for an estimated 35%+ of worldwide output

- India's pharmaceutical packaging sector represents a fast-growing niche for FDA-compliant TPE films, growing at ~9% annually

- Region expected to capture more than 40% of incremental global market demand through the forecast horizon

Conclusion

The Global TPE Films and Sheets Market is at a strategic inflection point, transitioning from a specialty materials segment into a mainstream industrial platform across automotive, packaging, medical, and consumer goods verticals. With market size at USD 3.4 billion in 2024, a projected trajectory to USD 5.1 billion by 2030, and R&D investment exceeding USD 1.5 billion, the sector is demonstrating both scale and innovation velocity. The convergence of EU recyclability mandates, EV-driven lightweighting imperatives, and Asia-Pacific manufacturing expansion creates a durable multi-vector growth story that is structurally differentiated from cyclical commodity polymer markets. Organizations across the value chain, from feedstock suppliers and compounders to film converters and end-use OEMs, face both competitive urgency and strategic opportunity in repositioning around high-performance, sustainable TPE film solutions.

Ken Research Finds

- Global TPE Films and Sheets Market valued at USD 3.4 billion in 2024, on track to reach USD 5.1 billion by 2030 at approximately ~7% CAGR

- Automotive sector alone to consume over 2 million tons of TPE films by 2030, making it the single largest end-use vertical globally

- R&D investment surpassing USD 1.5 billion is driving rapid advancement in bio-based, recyclable, and high-barrier TPE film formulations

- Asia-Pacific projected to grow 25% in TPE consumption, with China holding 35%+ of global production capacity

- EU Directive 2019/904 and FDA compliance mandates are reshaping procurement criteria for 85%+ of major polymer film buyer categories

- More than 22 global competitors active in the market, including BASF SE, Dow Inc., Covestro AG, Kraton Corporation, and Evonik Industries

- Biodegradable plastics adjacent market at USD 8 billion reflects scale of sustainability-driven materials transition benefiting TPE producers

- For deeper analysis of related polymer and specialty chemicals markets, explore Ken Research coverage of the Global FRP Recycling Market, UAE Specialty Ingredients Market, and Global Emollients Personal Care Market

Q1: What is the current size of the Global TPE Films and Sheets Market?

The Global TPE Films and Sheets Market was valued at USD 3.4 billion in 2024, according to Ken Research. The market is projected to grow at approximately ~7% CAGR through 2030, reaching an estimated USD 5.1 billion. This growth is anchored by demand from more than 4 major end-use sectors, with automotive and packaging collectively representing over 60% of total market volume. R&D investment in the sector exceeds USD 1.5 billion, indicating strong future innovation pipeline.

Q2: Which end-use sectors are driving TPE films demand most aggressively?

The automotive sector is the primary demand driver, with consumption projected to exceed 2 million tons by 2030, as EV platform proliferation accelerates lightweighting across 4+ vehicle sub-systems. Packaging ranks second, underpinned by the USD 1.2 trillion global packaging market's pivot toward flexible, recyclable films. Medical and healthcare applications are the fastest-growing niche, with India's pharmaceutical packaging segment alone expanding at approximately ~9% annually. Consumer goods complete the key demand quartet, particularly for TPE-based protective films and sealing applications where sustainability credentials command 15-20% pricing premiums.

Q3: What regulatory frameworks are shaping TPE film procurement decisions globally?

Three regulatory frameworks are structurally most impactful. EU Directive 2019/904 mandates recyclability for all single-use plastic items by 2030, directly advantaging certified TPE films over conventional thermosets. FDA compliance requirements govern food-contact packaging across North America, requiring documented safety profiles that command 15-20% pricing premiums. EPA standards in the US require lifecycle analysis documentation for industrial polymer films. Additionally, ISO certification is now required by 85%+ of automotive OEM procurement contracts for polymer film suppliers globally, creating meaningful compliance infrastructure barriers for smaller producers and consolidating share among the top 22 global competitors.

Q4: How is Asia-Pacific reshaping the global TPE films supply and demand balance?

Asia-Pacific is emerging as the defining regional force in the Global TPE Films and Sheets Market, with a projected 25% consumption increase through 2030. China currently holds an estimated 35%+ of global TPE film production capacity, supported by integrated feedstock availability and national advanced materials manufacturing policies. Japan and South Korea contribute precision-grade output for electronics and medical end-uses, where quality premiums are 20-30% higher than standard grades. India's packaging and healthcare verticals are growing at approximately ~9% annually, and the region as a whole is expected to capture more than 40% of incremental global market value addition through the forecast period.

Q5: What is driving R&D investment in next-generation TPE film formulations?

Total R&D investment in the TPE sector exceeds USD 1.5 billion globally, with USD 600 million specifically directed toward film and sheet product development. Three innovation vectors are attracting the most investment: bio-based TPE grades growing at approximately 2x the rate of conventional grades; high-barrier films for pharmaceutical and food packaging requiring sub-1 micron precision extrusion capabilities; and multi-layer co-extrusion architectures enabling 30%+ material reduction versus single-layer legacy designs. Regulatory compliance costs, particularly for EU and FDA-certified grades, are also accelerating consolidation investment, with the top 22 global players commanding disproportionate share of new capacity additions and IP protection in advanced film formulations.

Comments

Post a Comment