India Consumer Wearables Market Outlook 2024-2030: Growth Drivers and Forecast

India Consumer Wearables Market Outlook 2024-2030: Growth Drivers and Forecast

Executive Summary

India's consumer wearables market reached a turning point in 2024: unit shipments fell 11.3%, the first annual decline on record, even as category revenue held near USD 2.37 billion. Growth is shifting from volume to value as buyers trade up to premium devices.

Key Market Velocity Data

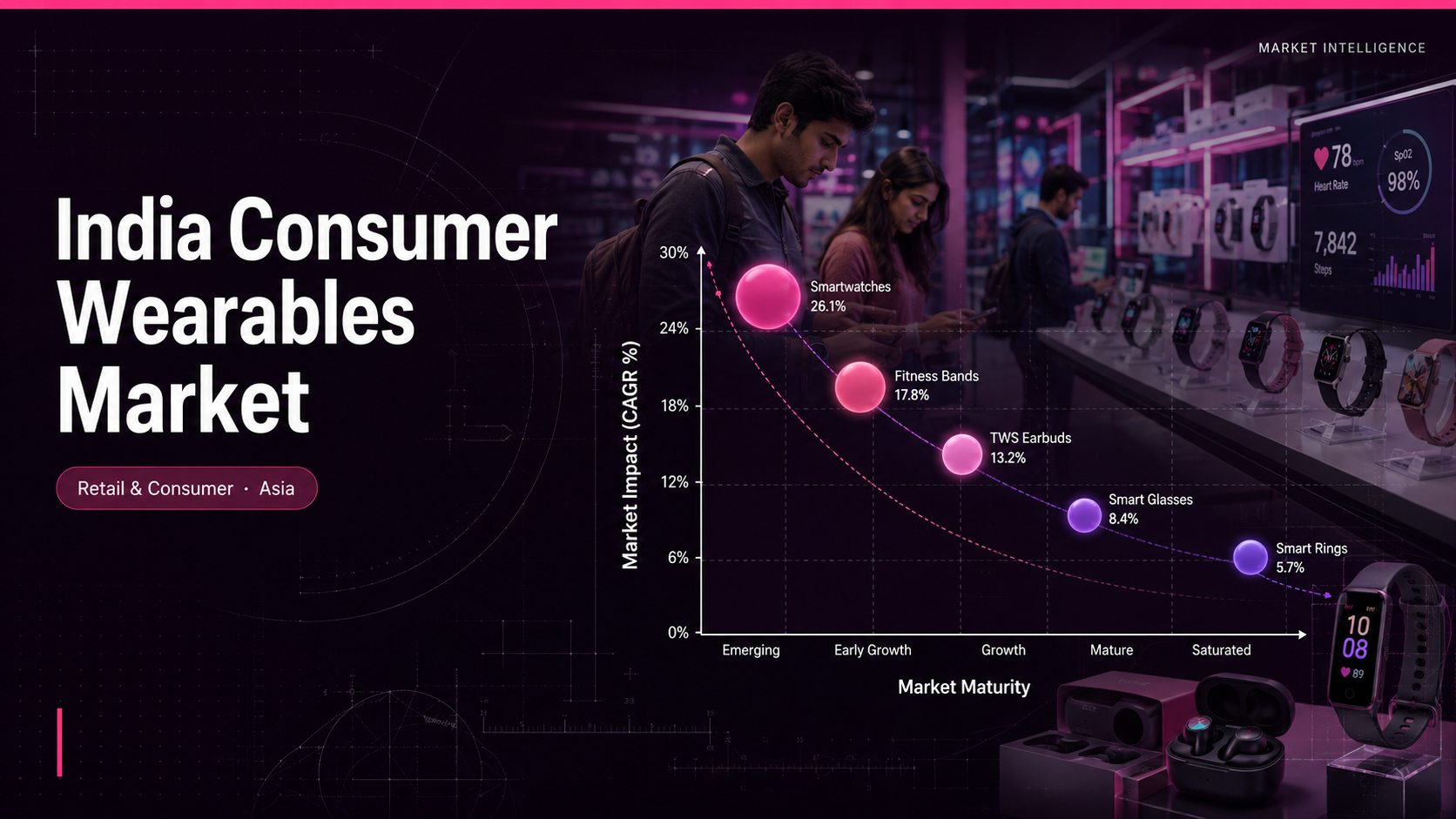

- Current Market Value: USD 2.37 billion in 2024

- Projected Market Value: approximately USD 7 billion by 2030

- CAGR: 19.4% during 2025 to 2030

- Dominant Regional Hub: South India and metro cities lead device revenue

- Primary Growth Catalyst: premiumization and rising health-tracking adoption

What Is Driving the Market?

The defining dynamic is value resilience against a volume contraction. India's wearable shipments peaked at 134.2 million units in 2023, then declined 11.3% in 2024, yet revenue held near USD 2.37 billion as average selling prices climbed.

The cheap-smartwatch wave that built the market has crested. Smartwatch shipments collapsed 34.4% in 2024, while TWS earbuds, a higher-loyalty category, grew 9.4%. Demand is concentrating in the 10,000 to 20,000 rupee band, where health sensors, brighter displays, and longer battery life justify premium pricing.

- Demand shift: TWS earwear grew 3.8% even as smartwatch shipments fell 34.4%, redirecting spend toward audio and premium watches

- Upgrade runway: penetration stays shallow by global standards, pulling first-time fitness-band owners toward feature-rich smartwatches above 10,000 rupee

- Supply-side change: offline channel shipments rose 7.2% while online fell 19.7% year over year

- Regulatory push: the Electronics Component Manufacturing Scheme, a 22,919 crore rupee programme, targets local batteries and displays through 2027

Which Entities Are Shaping the Market?

Consolidation is tightening at the top of a fragmenting base. boAt, operated by Imagine Marketing, led the overall wearables market with a 27.6% share in 2024, ahead of Noise (Nexxbase) at 12.2% and Boult at 8.6%.

The competitive picture diverges sharply by segment. In smartwatches, Noise extended its lead to 25.2% while Fire-Boltt slid to 16.7% and boAt fell to 11.8%. In TWS, boAt held firm at 34.2% as Boult expanded to 13.0%. Premium demand still routes to Apple, Samsung, and Titan's Fastrack.

On the supply side, the Ministry of Electronics and Information Technology, through its Production Linked Incentive scheme, and the Bureau of Indian Standards on import compliance, are reshaping where these devices are built and certified.

How Are Segments and Regions Splitting?

Segment and geography both concentrate the value pool. Fitness trackers and entry bands still drive volume, but smartwatches and TWS now carry the revenue, with the 10,000 to 20,000 rupee tier expanding fastest. South India leads fitness-tracker demand while metro cities deliver the highest revenue per device. Tier-2 and tier-3 cities form the next volume frontier, yet first-time buyers there increasingly skip basic bands for affordable TWS, reshaping the entry mix.

- Smartwatches: shipments fell 34.4% in 2024 yet the segment retains the highest selling price and feature attach rate

- TWS earbuds: grew 9.4% in 2024 with boAt at 34.2% and Boult the fastest riser at 13.0%

- Channels: offline grew 7.2% while online fell 19.7%, reversing the earlier e-commerce-led growth playbook for the category

What Does This Mean for B2B Decision-Makers?

The shift from volume to value rewrites go-to-market math. With 27 million units shipped in Q2 2025, down 9% year over year, scale alone no longer wins share profitably. The Q3 2024 drop of 20.7% to 38 million units showed how fast discount-led demand can evaporate.

Margin now sits in premium health features, durable brand trust, and offline distribution, which grew 7.2% even as online slipped 19.7%. For planners, the question moves from how many units to how much value each user delivers across the device lifecycle. Replacement cycles, not new-user acquisition, will set the pace, making after-sales service and software updates the real retention levers.

- For consumer electronics brands: prioritize premium smartwatch and TWS lines where prices are rising, not budget volume plays that drove the 34.4% smartwatch shipment fall

- For retail investors: weight exposure toward category leaders holding 27.6% and 12.2% overall share, since fragmentation is now reversing

- For procurement and channel teams: rebalance toward offline, which grew 7.2%, as online shipments fell 19.7% year over year

- For market entry teams: align component sourcing with the 22,919 crore rupee scheme to capture incentives before the 2027 window closes

Ken Research Strategic Outlook

Ken Research reads 2024 not as a slowdown but as the market's first maturity reset: the land-grab phase that pushed 134.2 million units in 2023 is over. The next cycle will be won on premiumization, health-data ecosystems, and locally manufactured margin rather than discount-led volume. As sub-scale brands exit, expect the top three to harden a combined hold above 48% of shipments, with value outpacing unit growth through 2030.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: India Consumer Wearables Market Report

Comments

Post a Comment