India Makhana Market Outlook 2024-2030: Growth, Exports, and Brand Competition

Executive Summary

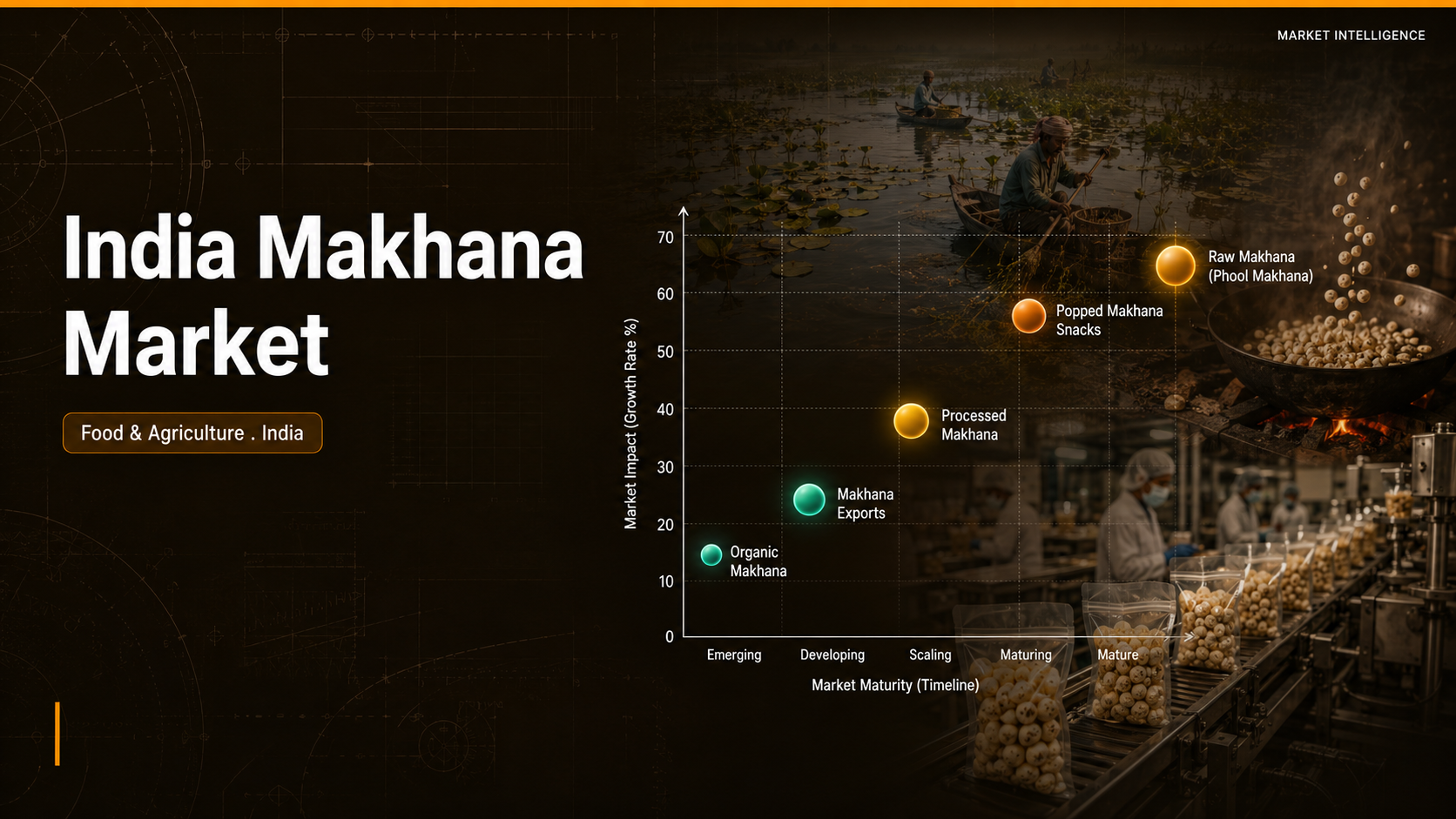

India's makhana market is scaling from a regional Bihar crop into a national superfood and a global export play. Health snacking, flavored innovation, and strong government backing are pushing the market from INR 100 Billion toward INR 240 Billion by 2030, reshaping sourcing and branding.

Key Market Velocity Data

- Current Market Value: INR 100 Billion in 2024

- Projected Market Value: around INR 240 Billion by 2030

- CAGR: 15.76% in value during 2024 to 2030

- Dominant Production Hub: Bihar, with over 80% of India's output

- Primary Growth Catalyst: health snacking and export demand

What Is Driving Demand in the India Makhana Market?

Demand is compounding on three fronts. Health snacking has gone mainstream, with about 40% of urban households shifting toward healthier options, and flavored makhana now makes up roughly 30% of urban sales. E-commerce carries close to 25% of makhana sales, while exports, still only 1% to 2% of total quantity, point to a large untapped global runway as diaspora and Western buyers adopt it as a clean-label popcorn alternative.

- Demand shift: about 40% of urban households moving to healthy snacks lifts makhana from festive niche to daily snack.

- Flavored growth: flavored variants now drive roughly 30% of urban sales, the fastest-premiumizing format.

- Channel change: e-commerce already carries close to 25% of sales, widening reach beyond traditional grocers.

- Export upside: exports sit at just 1% to 2% of volume, signaling a long runway as global demand builds.

How Do Government Policy and the GI Tag Shape the Market?

Government backing is unusually strong. The National Makhana Mission committed INR 500 crore from 2022, and Union Budget 2025-26 created a dedicated National Makhana Board with an initial INR 476 crore, alongside a National Makhana Research Centre. Bihar's 2026 subsidy scheme covers up to 75% of cultivation cost, supported by NABARD assistance for farmer producer organizations and APEDA export incentives (APEDA).

The Mithila Makhana GI tag, granted on August 16, 2022, lets certified farmers capture a 20% to 30% price premium in global markets. India already supplies over 90% of world makhana, and seed production reached 63.68 thousand tonnes in 2022, growing at a 13.24% CAGR over the prior decade.

Which Brands Are Shaping the Competitive Landscape?

The branded field is filling fast. Farmley raised USD 40 Million in Series C funding in May 2025, the largest round for a dedicated makhana brand, and has pushed into North American retail. Too Yumm, from the RP-Sanjiv Goenka Group, mainstreamed flavored makhana, while Tata Sampann, Haldiram's, and Patanjali leverage national distribution and brand recall.

Differentiation runs on flavor, packaging, and export reach. Mr. Makhana and MakhanaWala target the gifting niche, while Mithila Naturals, MeraKisan, and Farmley export to the USA, UK, UAE, Singapore, and Australia. With more than 15 active brands, shelf competition is intensifying faster than raw supply can formalize across Bihar's cultivation belt.

What Does This Mean for B2B Decision-Makers?

For processors, FMCG majors, and investors, makhana is shifting from commodity to branded category, and early positioning will define margin. With the market moving from INR 100 Billion toward INR 240 Billion by 2030 at a 15.76% value CAGR, the prize is large, but supply still depends on a Bihar base producing over 80% of output.

- For processors: invest in mechanized popping and grading, as over 90% of supply still relies on manual methods.

- For FMCG brands: build flavored and clean-label lines, the segment driving about 30% of urban demand.

- For exporters: target the USA and UAE early, since exports remain just 1% to 2% of volume.

- For investors: back funded scalers like Farmley, where USD 40 Million signals category consolidation.

Which Segments and Channels Lead the India Makhana Market?

Product and channel economics favor roasted and flavored formats sold off-trade. Roasted makhana holds the dominant share, flavored variants grow fastest, and raw and powder forms serve B2B ingredient buyers. Modern retail and e-commerce now anchor distribution, while gifting packs add a premium festive layer to the category.

- Product mix: roasted makhana leads, while flavored is the fastest-rising format at about 30% of urban sales.

- Channel split: e-commerce carries close to 25% of sales as quick-commerce widens access.

- Value addition: GI-certified Mithila makhana commands a 20% to 30% premium over ungraded supply.

Ken Research Strategic Outlook

The decisive lever in makhana is not demand, it is supply formalization. With India holding over 90% of global production from a largely manual Bihar base, the National Makhana Board and mechanization will decide how fast value migrates from raw seed to branded snack. Expect funded brands and exporters to capture the upside as the market doubles past INR 240 Billion by 2030, led by Bihar's gradually formalizing supply base.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: India Makhana Market Report

Comments

Post a Comment