Saudi Arabia Expanded Polyethylene Foam Market Outlook 2024-2030: Growth and Players

Executive Summary

Saudi Arabia's expanded polyethylene foam market is scaling on Vision 2030 construction and packaging demand. Lightweight protective packaging, megaproject insulation, and sustainability rules are pushing the market from USD 45 Million in 2024 toward roughly USD 73 Million by 2030, with non-cross-linked foam leading volume.

Key Market Velocity Data

- Current Market Value: USD 45 Million in 2024

- Projected Market Value: around USD 73 Million by 2030

- CAGR: about 8.5% during 2025 to 2030

- Largest End-User: packaging, with construction insulation rising fast

- Primary Growth Catalyst: Vision 2030 construction and packaging demand

What Is Driving Demand in the Saudi EPE Foam Market?

Demand is construction and packaging led. The Vision 2030 infrastructure pipeline exceeds USD 425 Billion, with megaprojects like NEOM and the Red Sea consuming over 500,000 tons of construction materials a year. The construction sector is growing about 6% annually, and industrial packaging demand has doubled from 260,000 to 650,000 tons over the past decade. Electronics exports, cold-chain logistics, and a fast-growing e-commerce sector add further protective-foam demand across the Kingdom.

- Megaproject demand: a USD 425 Billion pipeline drives insulation and protective-foam use.

- Construction growth: the sector expands about 6% a year, lifting foam insulation.

- Packaging surge: industrial packaging doubled from 260,000 to 650,000 tons.

- Sustainability pull: the sustainable-packaging market is projected near SAR 5 Billion.

How Do Standards and Sustainability Rules Shape the Market?

Regulation is steering material choices. The Saudi Standards, Metrology and Quality Organization sets product standards through its SALEEM safety program, while the Plastic Waste Management Rules of 2021 require minimum recycled content of 10% to 30% and extended producer responsibility (SASO). These rules push foam toward recyclable grades. Compliance now shapes which foam grades brands can specify, especially for export-bound sustainable packaging.

Vision 2030 reinforces the shift. Sustainability initiatives favor manufacturers that can meet recycled-content thresholds and certification, raising the bar for smaller producers. As SASO tightens life-cycle assessment, brand owners lock in longer-term supply contracts for certified polymers, supporting mid-single-digit price premiums. Local recycling capacity is expanding rapidly to meet these recycled-content mandates and reduce import reliance.

Which Companies Are Shaping the Competitive Landscape?

Integrated petrochemical majors anchor supply. SABIC supplies the polyethylene resin backbone, while Zamil Plastic Industries, founded in 1980 in Dammam, runs diversified plastics and announced a USD 45 Million automation program in 2025 targeting a 25% labor-cost cut by 2027. Al Watania Plastics adds packaging scale. Local resin integration gives Saudi producers a structural cost edge over importers exposed to volatile freight.

Specialist producers complete the field. National Petrochemical Company, Al-Jubail Petrochemical Company, Saudi Plastic Products Company, and Sealed Air Saudi compete across foam and protective packaging. The advantage sits with players that pair local resin access with recycled-content capability. Consolidation favors converters that combine manufacturing scale, automation, and certified recyclable grades.

What Does This Mean for B2B Decision-Makers?

For producers, packagers, and investors, the market is small but fast-growing and sustainability-gated, and recycled-content capability now decides margin. With the market moving from USD 45 Million toward roughly USD 73 Million by 2030 at about 8.5% CAGR, megaproject demand is the engine, but SASO compliance defines winners. Sustainability credentials are fast becoming a procurement requirement, not an optional differentiator, and export-grade certification opens GCC and European contracts.

- For producers: invest in recycled-content lines to meet the 10% to 30% thresholds.

- For packagers: target megaproject supply within the USD 425 Billion pipeline.

- For investors: back automation, as Zamil's USD 45 Million program shows the trend.

- For exporters: leverage local resin to displace imports across the GCC.

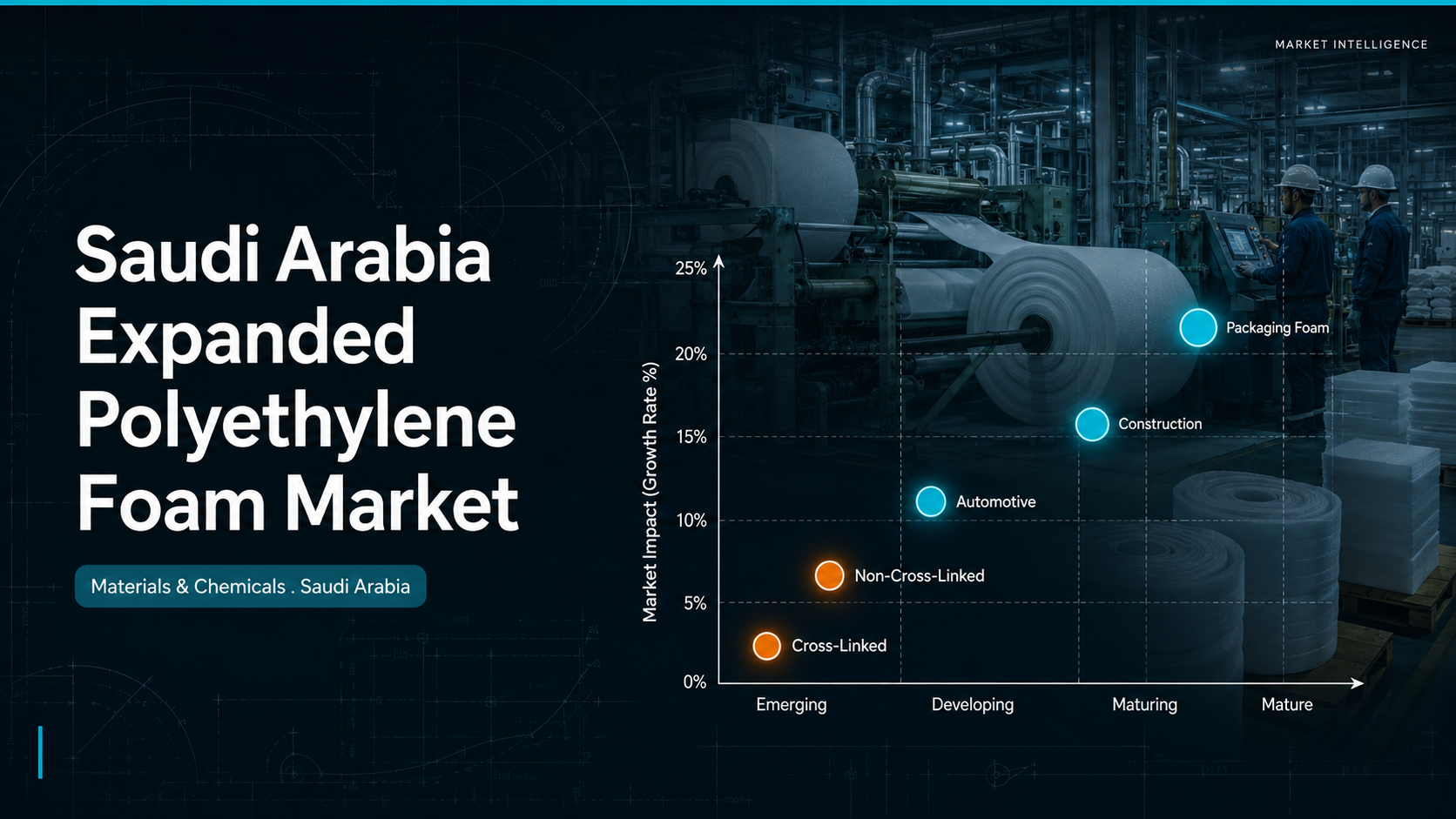

Which Segments and Applications Lead the Saudi EPE Foam Market?

Segment economics favor non-cross-linked foam in packaging and construction. Non-cross-linked EPE leads on cost and versatility, cross-linked foam serves premium automotive and technical uses, and construction insulation is the fastest-rising application. Packaging is the largest end-user, with automotive and electronics adding steady demand. Cold-chain and e-commerce packaging are the fastest-rising demand pockets for protective foam, while high-density grades command premium pricing in technical uses.

- Type mix: non-cross-linked EPE leads on cost, while cross-linked serves premium uses.

- Applications: packaging leads, with construction insulation the fastest-rising use.

- End users: automotive and electronics add steady protective-foam demand.

Ken Research Strategic Outlook

The decisive lever in Saudi EPE foam is Vision 2030 demand plus sustainability compliance, not raw price. As megaprojects scale and recycled-content rules tighten, margin will migrate toward integrated producers with local resin and certified, recyclable grades. Expect SABIC-backed players and automated converters like Zamil to lead, pushing the market toward USD 73 Million by 2030. Recyclable foam grades will increasingly displace conventional non-recyclable lines this decade.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Saudi Arabia Expanded Polyethylene Foam Market Report

Comments

Post a Comment