USA Goat Milk Products Market Outlook 2024-2030: Growth, Players, and Demand Signals

USA Goat Milk Products Market Outlook 2024-2030: Growth, Players, and Demand Signals

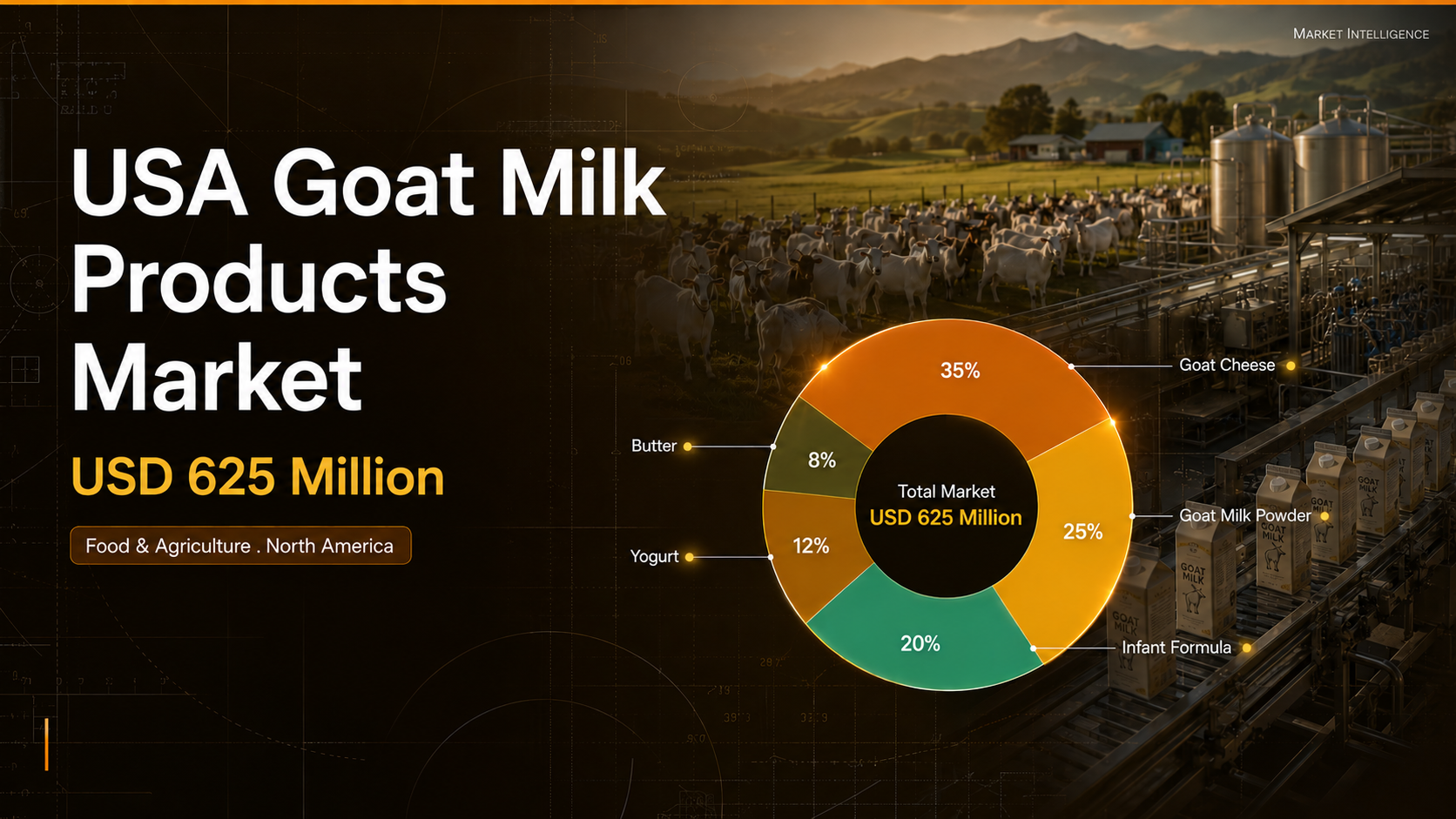

Executive Summary

US goat milk products are shifting from a niche specialty into a mainstream functional dairy category. Rising lactose intolerance and premium infant nutrition demand are pulling volume into goat cheese, powder, and formula, lifting the market toward USD 876 Million by 2030.

Key Market Velocity Data

- Current Market Value: USD 625 Million in 2024

- Projected Market Value: USD 876 Million by 2030

- CAGR: 4.9% during 2024 to 2030

- Dominant Production Hub: Midwest and West, with Wisconsin holding 74,000 milk goats

- Primary Growth Catalyst: lactose-free, organic, and infant-nutrition demand

What Is Driving Demand in the US Goat Milk Market?

Demand is moving on three measurable fronts. Lactose intolerance affects close to 36% of US adults, steering buyers toward goat milk, which carries smaller fat globules and far less A1 casein than cow milk. Goat cheese holds the dominant product share, while goat milk infant formula commands price premiums of 2x to 3x cow-based formula, making it the fastest-premiumizing segment in the category. Repeat-purchase rates on goat cheese signal durable demand, not a passing health fad.

- Demand shift: health-driven substitution, as lactose intolerance touches roughly 36% of adults, widens the addressable base well beyond specialty shoppers.

- Channel change: US online grocery scaling past USD 100 Billion is moving goat products out of 4 niche retail formats into mainstream e-commerce.

- Supply signal: USDA counted 415,000 milk goats on January 1, 2024, up 1% year over year, a slow base against accelerating demand.

- Regulatory push: the FDA Grade A PMO 2023 Revision raises compliance cost, tilting the category toward 3 to 4 scaled processors per line.

How Do Regulation and Regional Supply Shape the Market?

Production is regulated by the FDA under the Grade A Pasteurized Milk Ordinance 2023 Revision, which mandates pasteurization, a minimum 2.5% milk fat and 7.5% milk solids non-fat for retail goat milk, and microbial limits below 20,000 bacteria per mL (FDA milk regulation guidance). That load favors scaled processors over cottage producers, and new entrants must budget for pasteurization lines and state licensing before a single retail unit ships.

Supply is geographically concentrated. California, Texas, and New York lead licensed output, while Wisconsin alone holds 74,000 milk goats within a national herd of 415,000. Average yield has climbed to 1,901 pounds per 305-day lactation, a 9% gain over the 1,750 pounds recorded in 1996, yet herd expansion near 1% annually still limits how fast processors can scale fluid and powder supply.

Which Companies Are Shaping the Competitive Landscape?

The category is consolidating around a few branded processors. Meyenberg Goat Milk anchors powdered and fluid goat milk nationally, and Redwood Hill Farm and Creamery, now under Emmi Group following its 2016 acquisition, leads goat yogurt and kefir. Mt. Capra Products and Woolwich Dairy hold premium cheese and nutrition positions across specialty retail, competing on provenance, herd-welfare claims, and clean-label positioning rather than price alone.

That concentration leaves limited room for unbranded entrants. Private-label players chase the remaining shelf share, but the 5 core product lines, from cheese to infant formula, are increasingly defined by incumbents with secured farm supply, making brand and milk access the two real barriers to entry. Emmi Group's ownership of Redwood Hill shows how foreign dairy majors buy into US goat brands rather than build herds from scratch.

What Does This Mean for B2B Decision-Makers?

The category is crossing from artisan to scalable, and capacity decisions made now will set margin for the decade. With the market moving from USD 625 Million toward USD 876 Million by 2030, the volume is real but constrained by a 415,000-head milk-goat base growing near 1% a year, which keeps upstream milk the scarcest input. Buyers that move early on supply will hold pricing power as demand compounds.

- For processors: lock multi-year milk-supply contracts now, since herd growth near 1% lags demand growth of 4.9%.

- For retail buyers: expand goat cheese and infant-formula facings, the two highest-velocity segments, ahead of 2030.

- For investors: target branded infant-formula assets, where price realization runs 2x to 3x fluid goat milk.

- For market-entry teams: prioritize the West and Midwest, where Wisconsin's 74,000 milk goats and established plants anchor supply.

Ken Research Strategic Outlook

The decisive constraint in US goat dairy is not consumer demand, it is herd supply. With milk-goat inventory expanding near 1% annually against demand near 5%, margin will migrate toward vertically integrated players that secure farm-level milk before rivals. The infant-formula segment, shielded by regulatory barriers and premium pricing of 2x to 3x, should resist private-label compression the longest, while commodity fluid milk stays the most exposed. Expect selective M&A as distributors acquire regional cheese and formula brands.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: USA Goat Milk Products Market Report

Comments

Post a Comment