APAC Military Actuators Hits USD 1.2 Billion : Ken Research Finds DAP 2020 and Automation Drive 6.1% CAGR

APAC Military Actuators Market Crosses USD 1.2 Billion in 2024: Ken Research Finds Defense Automation and Smart Actuation Driving 6.1% CAGR Through 2030

Executive Summary

While global defense supply chains scramble to reduce strategic dependency on foreign-sourced components, Asia Pacific is building the region's most consequential precision actuator ecosystem. Ken Research values the APAC Military Actuators Market at USD 1.2 billion in 2024, projected to reach USD 1.7 billion by 2030 at a 6.1% CAGR. India's Defense Acquisition Procedure (DAP) 2020 mandates higher indigenization of defense components, and China's accelerating rearmament programs are restructuring OEM procurement pipelines across the region. For full data, see the APAC Military Actuators Market Research Report.

Analyst: Ken Research Market Analysis | Methodology: Ken Research market modelling, defense ministry procurement data, OEM manufacturer disclosures, operator interviews, and regulatory filings across China, India, Japan, and South Korea.

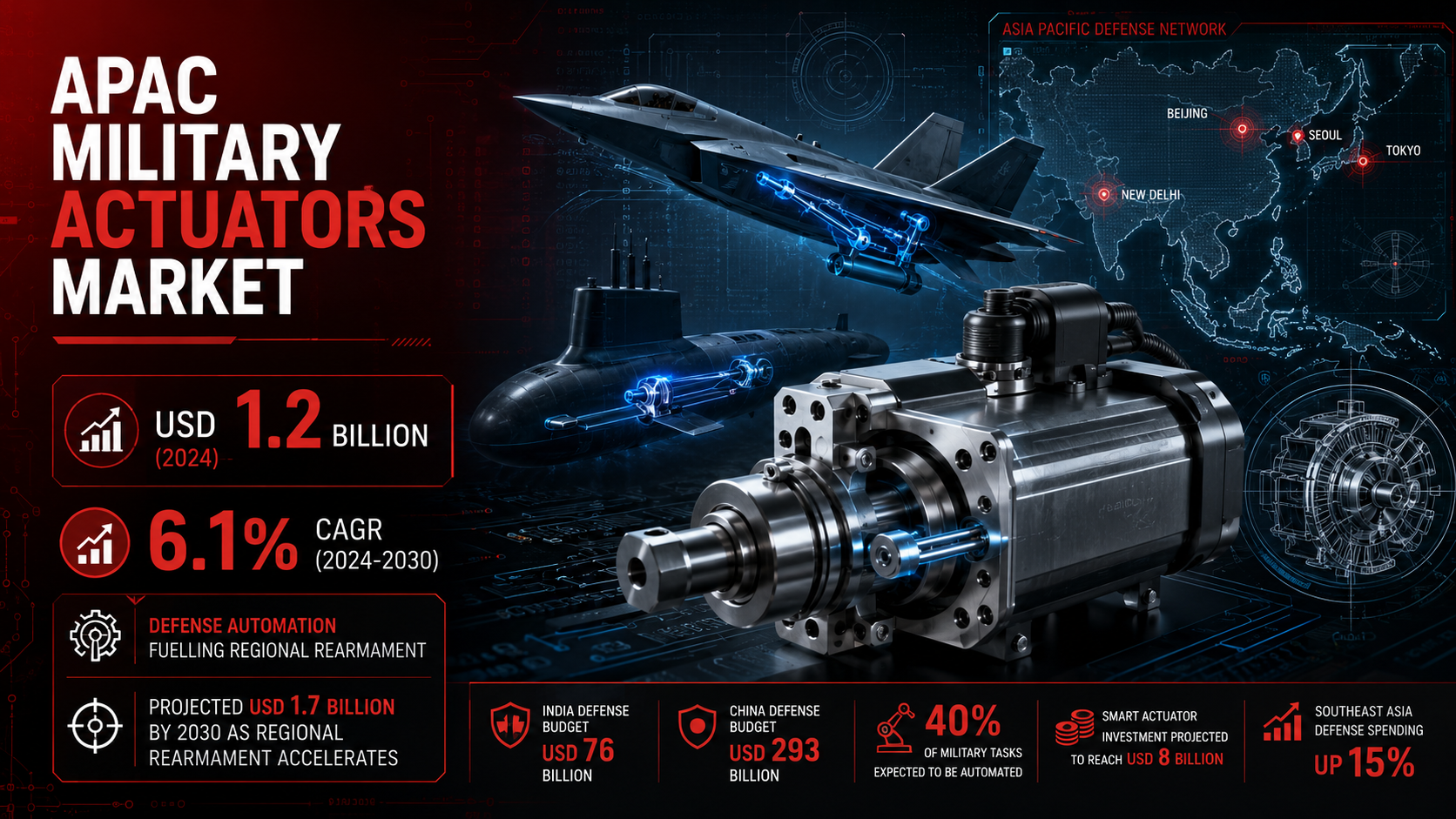

Key Takeaways

- Market Valuation 2024 (Ken Research): USD 1.2 billion reflecting consolidated procurement across ground, naval, and airborne platforms spanning six APAC sub-regions including Southeast Asia and Oceania.

- Growth Trajectory 2024-2030 (Ken Research): 6.1% CAGR sustained by platform modernization, UAV proliferation, and electromechanical actuator adoption replacing legacy hydraulic systems.

- Indigenization Mandate (India Ministry of Defence, DAP 2020): Higher domestic sourcing requirements forcing actuator OEMs to establish local manufacturing partnerships or face contract exclusion from Indian tenders.

- Competitive Structure (Ken Research): Honeywell International, Moog Inc., and Parker Hannifin lead APAC supply, with Bharat Electronics Limited and Hanwha Aerospace gaining ground through government-linked contracts.

- Automation Acceleration (Ken Research): 40% of military tasks expected to be automated, with smart actuator investments projected at USD 8 billion creating near-term procurement windows.

Market At A Glance

Market Size and Growth Trajectory

Ken Research values the APAC Military Actuators Market at USD 1.2 billion in 2024, projected to reach USD 1.7 billion by 2030 at 6.1% CAGR, driven by sustained defense budget expansion and platform modernization. China's defense outlay is projected at USD 293 billion and India's at USD 76 billion (Ken Research), with both nations prioritizing domestic actuator procurement chains. The Indonesia Defense Market adds sub-regional naval and ground vehicle procurement volume, reinforcing ASEAN's emergence as a third actuator demand corridor alongside China and India.

Competitive Landscape

Honeywell International leads APAC at an estimated 12-15% regional share (Ken Research), followed by Moog Inc. at 10-12% and Parker Hannifin at 8-10%. Domestic challengers BEL, Hanwha Aerospace, and Mitsubishi Heavy Industries are consolidating government contracts requiring localization. NORINCO and Nanjing High Accurate Drive (NGC) dominate China's domestic pipeline. The Indonesia Aerospace Defense MRO Market represents a growth corridor for actuator aftermarket servicing and platform maintenance across Southeast Asia's expanding naval and air fleets.

Why 40% Military Automation Is Not a Forecast: It Is the Procurement Floor Actuator OEMs Must Design For Now

Defense procurement officers across APAC are specifying autonomous capability thresholds into current tender documentation, not future roadmaps. Ken Research estimates 40% of military tasks expected to be automated, with smart actuation investment projected at USD 8 billion (Ken Research). Development costs for specialized military actuator projects exceed USD 10 million per project (Ken Research), creating qualification barriers that favor incumbent suppliers with MIL-SPEC certifications. This is not a ceiling; it is the design baseline for every platform entering active procurement. The Global Collaborative Robot Market and military automation share the same electromechanical actuation architecture, enabling dual-use procurement strategies for OEMs seeking to serve both defense and industrial channels. By 2029, Ken Research projects smart actuators to represent 30% of total APAC military actuator units versus under 15% in 2024.

- Rotary Actuators: Largest current segment share across airborne and naval platforms, with electromechanical variants displacing hydraulic in fighter jet control surfaces (Ken Research).

- Smart Actuators: USD 8 billion investment projection signals AI-integrated actuation with real-time fault detection transitioning to standard tender specification (Ken Research).

- Electromechanical Technology: Highest growth sub-segment preferred for UAV and UGV platforms where weight and digital control determine mission viability (Ken Research).

Evaluating supplier positioning or OEM partnership strategy in APAC military actuation? Download Sample Report for competitive analysis and segment strategy.

The USD 293 Billion Signal: Why China and India Are Rewriting APAC Actuator Supply Chain Architecture

China and India are not merely growing defense budgets; they are systematically closing procurement pipelines to external suppliers without localized operations. R&D investment across APAC is projected at USD 15 billion in advanced military technologies (Ken Research), with substantial portions flowing into precision actuation, sensor fusion, and autonomous control systems. Southeast Asia defense spending is projected to increase by 15%, adding procurement depth beyond the China-India core (Ken Research). The Japan Aerospace and Defense Market navigates this through its Five-Year Defense Reinforcement Plan, generating actuator demand for next-generation fighter programs and destroyer fleet upgrades where localized supply chains are now a program requirement, not a preference. By 2030, China and India together are projected to account for over 65% of total APAC military actuator procurement value (Ken Research).

- China Defense Procurement: USD 293 billion projected outlay with NORINCO and NGC holding captive domestic supply positions closed to foreign OEMs without localized operations (Ken Research).

- India DAP 2020: USD 5 million annual compliance cost creates effective localization tax on foreign suppliers, accelerating BEL and domestic tier-2 manufacturers (India Ministry of Defence, DAP 2020).

- R&D Pipeline: USD 15 billion projected in APAC advanced military technology R&D, creating upstream demand for precision actuator prototyping and qualification services (Ken Research).

Conclusion

The APAC Military Actuators Market grows from USD 1.2 billion (2024) to USD 1.7 billion (2030) at 6.1% CAGR, driven by surging regional defense budgets, UAV proliferation, electromechanical actuator adoption, and indigenization mandates reshaping supply chain architecture. OEMs without established localization strategies face progressive contract exclusion against a backdrop of USD 15 billion in regional R&D investment (Ken Research). The India Drone Manufacturing and Applications Market and Southeast Asian volumes add a third growth corridor beyond the China-India duopoly. The Thailand Drone Delivery and UAV Logistics Market reflects how civilian drone infrastructure upgrades feed military-grade actuator ecosystem development across ASEAN.

Validating supplier or platform entry strategy for APAC defense actuator procurement? Request APAC Military Actuators Market Intelligence to validate strategy.

Frequently Asked Questions

Q1: What is the APAC Military Actuators Market size and growth rate?

Ken Research values the APAC Military Actuators Market at USD 1.2 billion in 2024, projected to reach USD 1.7 billion by 2030 at a 6.1% CAGR. The market is driven by China and India's defense expansions and a regional shift toward electromechanical and smart actuation platforms. The India Robotics and Automation in Manufacturing Market provides the precision manufacturing base supporting defense actuator growth.

Q2: Which companies lead the APAC Military Actuators Market?

Ken Research analysis identifies Honeywell International (12-15% regional share), Moog Inc. (10-12%), and Parker Hannifin as dominant foreign OEMs, alongside domestic champions BEL, Hanwha Aerospace, and Mitsubishi Heavy Industries consolidating government-linked contracts under active indigenization programs. The Indonesia Aerospace Defense MRO Market provides aftermarket servicing demand complementing OEM supply positions across Southeast Asia's expanding defense fleets.

Q3: What is the APAC Military Actuators Market outlook through 2030?

Ken Research projects the market growing from USD 1.2 billion (2024) to USD 1.7 billion (2030) at 6.1% CAGR, driven by platform modernization, UAV fleet expansion, smart actuator adoption, and Southeast Asia defense spending rising 15%. Rotary actuators currently hold the largest segment share across airborne applications, while electric and smart actuators are gaining platform share across next-generation UAV programs in Japan and South Korea.

Q4: What regulatory factors shape APAC Military Actuators adoption?

According to India's Ministry of Defence, the Defense Acquisition Procedure (DAP) 2020 mandates higher indigenization of all defense components, with annual compliance costs at USD 5 million per manufacturer, directly forcing actuator OEMs to localize or exit Indian procurement pipelines. China's parallel policy maintains domestic content imperatives for all PLA procurement. The Saudi Arabia Military Tactical Radio Market illustrates how comparable certification requirements entrench supplier relationships in analogous defense procurement ecosystems.

Q5: What efficiency gains do smart military actuators deliver versus legacy hydraulic systems?

According to Ken Research, electromechanical and smart actuator implementations deliver 20-35% reductions in maintenance cycles versus legacy hydraulic systems, with weight savings of 15-25% enabling UAV payload and range improvements critical to mission profiles. Smart actuators with AI-based fault detection reduce unplanned platform downtime by an estimated 40%, directly improving readiness KPIs. The Global Industrial Valves and Actuators Market documents the commercial-grade performance benchmarks that military-grade smart actuator specifications are now expected to exceed across APAC procurement programs.

Comments

Post a Comment