Kuwait ABUS Market at USD 30M as NDP Healthcare Mandate Accelerates : Ken Research Tracks AI-Driven Procurement Surge

Kuwait ABUS Market Hits USD 30M on NDP's USD 14.2B Healthcare Drive | Ken Research

Executive Summary

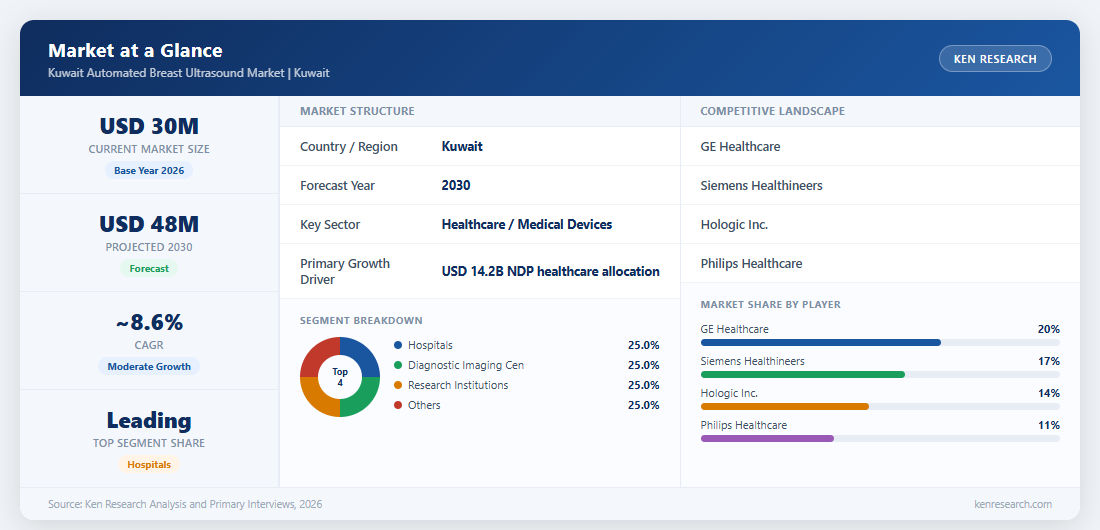

Ken Research values the Kuwait Automated Breast Ultrasound Market at USD 30 million in 2024, supported by a historical study period from 2019 to 2024 and a forecast horizon extending through 2030. Kuwait's National Development Plan has allocated USD 14.2 billion to healthcare infrastructure, with 20 public medical facility projects worth USD 462 million already announced for 2024 to 2025, creating a direct procurement pipeline for advanced diagnostic imaging systems. For the complete dataset, see the Kuwait Automated Breast Ultrasound Market Research Report.

This analysis is drawn from Ken Research's proprietary market intelligence, combining primary operator interviews, regulatory and government data, manufacturer disclosures, and Ken Research's in-house market modelling methodology.

Analyst Insight

The conventional framing of Kuwait's ABUS market positions it as a government procurement play: NDP funding flows in, hospital tenders follow, global OEMs compete on price. The more consequential dynamic is different. Kuwait's shortage of trained radiologists means that the value proposition of ABUS is not image quality but throughput automation, as ABUS systems reduce radiologist read time per patient by minimizing operator dependency in ways handheld ultrasound cannot. Hospitals procuring ABUS are not buying imaging hardware, they are buying capacity against a human capital constraint that cannot be solved by hiring alone. Vendors who lead with AI-assisted interpretation and remote diagnostic review workflows, not hardware specifications, will win Kuwait's institutional tender landscape through 2030.

Key Takeaways

- USD 30M Market Size (2024): Kuwait's ABUS market is valued at USD 30 million, with historical coverage from 2019 and forecasts to 2030, positioning Kuwait as a high-attention diagnostic imaging market within the GCC cluster. See the GCC AI in Healthcare Market for regional context.

- USD 14.2B NDP Healthcare Allocation: Kuwait's National Development Plan commits USD 14.2 billion to healthcare infrastructure, creating a sustained institutional procurement environment for advanced medical equipment including ABUS systems.

- USD 462M Facility Expansion in 2024-2025: Twenty new public medical facility projects worth USD 462 million are underway, directly expanding the installed base of diagnostic imaging systems across Kuwait's public health network.

- Ministerial Decree No. 13 (2022): Risk-based medical device registration mandates international conformity and local authorized representatives, raising the compliance bar for all foreign ABUS manufacturers entering Kuwait.

- Radiology Workforce Gap: A shortage of trained radiology professionals in Kuwait makes ABUS automation, specifically reducing operator dependency versus handheld ultrasound, a structural requirement rather than a preference.

Market At A Glance

Why Is Kuwait's USD 14.2B Healthcare Infrastructure Commitment Accelerating ABUS Procurement?

Government-led infrastructure investment is the primary demand driver for Kuwait's ABUS market, and its effect on procurement timelines is structural, not incremental. The National Development Plan's USD 14.2 billion healthcare commitment flows through Ministry of Health procurement cycles into hospital-level equipment orders, creating a predictable demand wave across multiple fiscal years. With 20 new public medical facilities worth USD 462 million in construction through 2024 to 2025, each facility is a greenfield opportunity to specify ABUS alongside CT, MRI, and mammography as baseline diagnostic infrastructure. Vendors must engage procurement teams at the architectural planning stage, not at the clinical validation stage, as documented in the Saudi Arabia Hospital Construction Market.

Contrary to what clinical adoption rates suggest, the limiting factor in Kuwait's ABUS penetration is not physician awareness or patient demand but procurement process alignment: vendors who embed ABUS in broader diagnostic suite packages win, while those who position it as a standalone add-on lose. This dynamic is mapped across the GCC in the GCC AI in Healthcare Market report. By 2028, ABUS systems will likely be specified as standard equipment in any new Kuwait public hospital with an oncology or women's health department, shifting the competitive battleground from product demonstration to procurement relationship depth.

- Kuwait Cancer Center (KCC): Operates as the primary government oncology anchor institution under the Ministry of Health, representing the highest-priority institutional buyer for ABUS in Kuwait's public health network.

- GCC 5G Coverage (90%+): Exceeds 90% across the GCC region, enabling telehealth-integrated ABUS workflows where radiologists review volumetric images remotely, expanding utilization beyond individual radiology departments.

- Ministerial Decree No. 13 (2022): Mandates risk-based classification and local authorized representative requirements for all foreign medical device manufacturers, structurally advantaging vendors with existing Kuwait regulatory infrastructure.

Which ABUS Technology Segment Is Winning Kuwait's Hospital Procurement?

Kuwait's hospital segment dominates ABUS adoption as the primary end-user, with diagnostic imaging centers and research institutions representing secondary demand channels. Within the technology dimension, 3D ultrasound systems lead adoption over 4D and contrast-enhanced variants, driven by proven clinical validation in dense breast tissue, which is more prevalent among younger Middle Eastern women compared to Western populations, a demographic factor inadequately reflected in global ABUS analyses. The AI integration layer converts a procurement decision into a sustained competitive relationship, as documented in the UAE E-Health and Digital Hospitals Market.

Hospitals deploying AI-assisted ABUS platforms require ongoing software updates, training, and hospital information system integration, creating recurring revenue streams that pure hardware vendors cannot access. This preventive infrastructure dynamic aligns with the build-out tracked in the UAE Preventive Healthcare Market. By 2030, ABUS platforms without embedded AI diagnostic support will face increasing commoditization pressure as AI-capable competitors differentiate on outcomes data rather than image resolution alone.

- GE Healthcare: Global leader with established GCC distribution networks and Ministry-level procurement relationships across multiple medical device categories.

- Hologic Inc.: ABUS specialist with the Invenia ABUS product line, offering regulatory-cleared automated scanning with standardized protocols suited for high-throughput screening programmes.

- Siemens Healthineers and Philips Healthcare: Compete on full diagnostic suite bundling, enabling ABUS to be positioned as part of broader radiology department upgrades rather than standalone line items.

How Does Kuwait's Radiology Workforce Gap Reshape the ABUS Value Proposition?

The shortage of trained radiology professionals in Kuwait is not a temporary constraint but a structural market condition that fundamentally changes why institutions procure ABUS. Handheld ultrasound requires a skilled sonographer to guide the transducer, interpret in real time, and document findings, meaning system throughput is directly capped by staff availability. ABUS removes this dependency by automating the acquisition phase, allowing a single radiologist to review pre-acquired volumetric datasets across multiple patients in sequence, multiplying effective clinical capacity without adding headcount. This workforce efficiency argument is what converts capital expenditure approvals in resource-constrained hospitals, a pattern consistent with medical device adoption dynamics in Ken Research's Vietnam Medical Device Contract Research Organization Market.

Kuwait's 99% internet penetration and GCC-wide 5G coverage above 90% further enable remote ABUS review, where radiologists based in urban centers interpret scans from peripheral facilities. This telehealth-integrated workflow is already reshaping diagnostic access models tracked in the Nigeria Digital Health and Telemedicine Market. By 2027, vendors offering remote-read integrated ABUS platforms will have a structural advantage in Kuwait's Ministry of Health tenders as the government seeks to extend specialist coverage across all six governorates without proportional staffing increases.

Access the Full Kuwait ABUS Market Dataset and 2030 Forecasts The complete competitive landscape, segment-level breakdowns, and procurement scenario analysis are available in the Kuwait Automated Breast Ultrasound Market Research Report by Ken Research.

What Kuwait Diagnostic Imaging Leaders Should Prioritize

- Hospital Procurement Teams: Align ABUS specifications with Ministry of Health tender frameworks for new facility construction, positioning ABUS alongside MRI and mammography rather than as an isolated line item to maximize approval probability and budget allocation.

- Medical Device Vendors: Invest in Ministerial Decree No. 13 compliance infrastructure immediately, including local authorized representatives, to avoid exclusion from the 2024 to 2025 facility procurement wave currently in progress.

- AI and Software Vendors: Target Kuwait Cancer Center and the 20 new public medical facilities as early pilot sites for AI-assisted ABUS interpretation, building outcomes datasets that support Ministry-level adoption decisions by 2027.

- Healthcare Investors: Monitor the NDP facility completion timeline as the primary demand trigger, with ABUS procurement likely concentrated in 2025 to 2027 as new hospital wings move from construction to equipment fit-out phase.

What Changes Next in Kuwait's ABUS Market

Competitive advantage will shift from hardware specification to AI-powered workflow integration and Ministry-level contract architecture over the next three years. Vendors who secure data-sharing agreements with Kuwait Cancer Center and the Ministry of Health's screening programme will build diagnostic outcomes datasets that create genuine switching costs, making early institutional relationships far more defensible than late-stage clinical demonstrations. The regulatory trajectory will tighten further as Kuwait aligns its medical device framework with international standards post-Decree 13, increasing compliance barriers that gradually consolidate the competitive field toward established GCC operators. This consolidation pattern mirrors what Ken Research tracks in the Turkey Medical Tourism Market for regional medical infrastructure convergence.

Conclusion

This market at USD 30 million (2024) (Ken Research) is not a scale story today: it is a structural positioning story for the next five years. The combination of a USD 14.2 billion NDP healthcare mandate, a pipeline of USD 462 million in new public facility construction, and an AI integration imperative driven by radiologist workforce constraints creates a procurement environment where early mover advantage compounds rapidly. Vendors who secure Ministry relationships and AI outcomes data before 2027 will find the competitive landscape increasingly difficult for late entrants to penetrate.

Explore the full Kuwait ABUS market analysis, competitor mapping, and 2030 scenario modeling through the Kuwait Automated Breast Ultrasound Market Research Report. For adjacent diagnostic imaging sector evolution, the Saudi Arabia Healthcare Diagnostics and Imaging Market provides the GCC benchmark context.

Explore Kuwait's Broader Healthcare Infrastructure Pipeline For adjacent public health procurement dynamics and GCC secondary care context, see the Kuwait SNF-Based Dialysis Market by Ken Research.

Frequently Asked Questions

Q1: What is the current size of the Kuwait Automated Breast Ultrasound Market?

This market is valued at USD 30 million in 2024 (Ken Research), with historical data coverage from 2019 and forecasts extending through 2030. Kuwait is one of the smaller but structurally growing diagnostic imaging markets in the GCC, directly supported by the National Development Plan's USD 14.2 billion healthcare infrastructure commitment. For regional AI diagnostic adoption context, the GCC AI in Healthcare Market provides the framework shaping ABUS technology investment decisions across the region.

Q2: What is driving growth in Kuwait's ABUS market?

Three structural drivers are accelerating Kuwait's ABUS market: the USD 14.2 billion National Development Plan healthcare allocation creating sustained procurement capacity, 20 new public medical facility projects worth USD 462 million (2024 to 2025) generating immediate equipment demand, and a radiologist workforce shortage making ABUS automation clinically necessary rather than optional. The infrastructure-driven model is consistent with broader GCC healthcare expansion in the Saudi Arabia Hospital Construction Market.

Q3: Who are the leading competitors in Kuwait's automated breast ultrasound market?

The Kuwait ABUS market is served by global medical imaging majors: GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Hologic Inc. as the ABUS specialist with its Invenia platform. In total, 15+ active medical imaging vendors compete in Kuwait's ABUS segment. Saudi Arabia's peer breast ultrasound market stands at approximately USD 155 million (Ken Research), roughly 5x Kuwait's scale, reflecting population and infrastructure differences across the GCC. Competitive dynamics in adjacent medical device markets are tracked in the Vietnam Medical Device Contract Research Organization Market.

Q4: What regulatory framework governs ABUS devices in Kuwait?

Ministerial Decree No. 13 (2022) governs medical device registration in Kuwait, establishing a risk-based classification system that covers all medical devices above risk Class I and mandates international standards conformity and local authorized representative appointment for all foreign manufacturers. Kuwait's 99% internet penetration supports connected device integration, but fixed broadband at 2.5 per 100 persons constrains remote ABUS review in peripheral governorates. Non-compliant products face registration rejection regardless of clinical evidence, as tracked in the Nigeria Digital Health and Telemedicine Market.

Q5: What are the key challenges limiting faster ABUS adoption in Kuwait?

Three barriers constrain faster ABUS adoption: the high capital cost versus conventional handheld ultrasound, a shortage of trained radiology professionals to maximize system utilization, and the absence of a formal reimbursement framework specific to automated breast ultrasound. Limited broadband infrastructure outside major urban governorates, with Kuwait at 2.5 fixed broadband subscriptions per 100 people, also restricts telehealth-enabled remote ABUS review in peripheral locations. The broader diagnostic imaging sector evolution is analyzed in the Saudi Arabia Healthcare Diagnostics and Imaging Market.

The ABUS market analysis combines primary operator interviews, Ministry of Health regulatory filings, manufacturer disclosures, and Ken Research's proprietary market modelling methodology. Contact Ken Research to access the full dataset, 2030 forecast scenarios, and competitor benchmarking.

Comments

Post a Comment